Mon to Sat From 9:00AM to 9:00PM | Download Brochure | Client Login |

Mon to Sat From 9:00AM to 9:00PM | Download Brochure | Client Login |

On April 23, 2020, one of the largest Asset Management Company – Franklin Templeton announced winding-up of six of its Debt Funds Schemes resulting in shaking the confidence of the investor in the mutual fund market. The schemes entrusted to the trustees i.e. Franklin Templeton Trustee Services Pvt. Ltd (hereinafter referred to as the Trustees) and managed through Franklin Templeton Asset Management (India) Pvt. Ltd. (hereinafter referred to as the Asset Management Company or the AMC) which were wound-up are as follows:

1. Franklin India Ultra Short Bond Fund (FIUBF)

2. Franklin India Short Term Income Fund (FISTIP)

3. Franklin India Credit Risk Fund (FICRF)

4. Franklin India Low Duration Fund (FILDF)

5. Franklin India Dynamic Accrual Fund (FIDA)

6. Franklin India Income Opportunities Fund (FIIOF)

Such an unprecedented action taken by one of the largest companies with ample expertise in the field had created a panic amongst the middle class investors who had put in their savings into the schemes in hope for higher returns. In such a scenario, the only question haunting the minds of the investor is what can be done to get their money back as soon as possible?

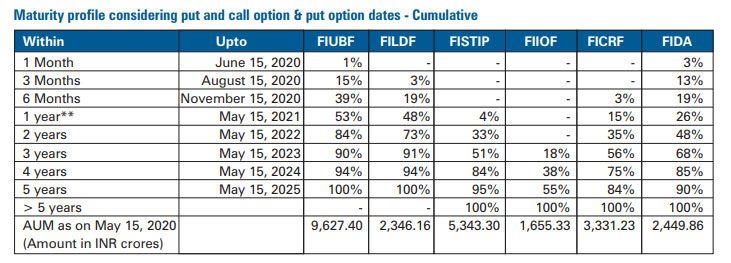

As per the maturity profile of the schemes uploaded on the website of Franklin Templeton, the cash flow projections basis portfolio holdings as on May 15, 2020 are as follows: 1

Meaning thereby, that for the investors to get their money back, even in case of Ultra Short Bond Fund, they’ll have to wait for a period of 5 years. It is to be noted that the average maturity of Franklin Ultra Short Bond Fund is 0.62 years or about 7.5 months. For Franklin Low Duration, Franklin Short Term Income, Franklin Dynamic Accrual, Franklin Income Opportunities and Franklin Credit Risk that average maturities are 1.46, 2.75, 4.28, 2.55 and 3.08 years (as of 31st March 2020) 2. Thus, such a long wait coupled with the silence of the government regulatory is slowly eroding away the trust of the Indian investor in the mutual fund market. Given the first-time occurrence of such an event, let us first examine the Legality of the winding-up.

Franklin Templeton without sending any personal intimation to the unit-holders in various schemes, through email or otherwise, had issued a Notice3 dated 23.04.2020 which had been uploaded on the official website purported to be issued pursuant to Regulation 39(2)(a) of the SEBI (Mutual Fund) Regulations, 1996 4 (hereinafter referred to as the MF Regulations). The notice neither discloses the name of the person who has signed it nor refers to the date, place or number of any resolution that has been passed by the trustees. It is also stated that no member of the Board of Trustees has ever appeared in any media briefing. All the subsequent emails, if any, to the investors relating to the voting process and also certain documents relating the winding-up have been signed by Mr. Sanjay Sapre, President of Franklin Templeton Asset Management (India) Pvt. Ltd. But he holds no office in the Trustee Company.

Assuming without admitting, that the Trustees had issued the Notice dated 23.4.2020 informing the board and the general public of a purported exercise of power under Regulation 39(2)(a) which enables the trustees to wind up a scheme on the happening of any event which, in the opinion of the trustees, requires the scheme to be wound up. The said regulation is reproduced below for ready reference:

"39. Winding-up:

2https://www.livemint.com/money/personal-finance/10-faqs-about-the-freeze-in-franklin-templeton-debt-schemes-11587702160321.html

3https://www.franklintempletonindia.com/downloadsServlet/pdf/notice-of-winding-up-final-230420-k8lf815l

4https://www.sebi.gov.in/sebi_data/commondocs/mutualfundupdated06may2014.pdf

(2) A scheme of a mutual fund may be wound up, after repaying the amount due to the unit holders,-

(a) on the happening of any event which, in the opinion of the trustees, requires the scheme to be wound up; or …

(3) Where a scheme is to be wound up under sub-regulation (2), the trustees shall give notice disclosing the circumstances leading to the winding up of the scheme:—

(a) to the Board; and

(b) in two daily newspapers having circulation all over India, a vernacular newspaper circulating at the place where the mutual fund is formed."

It is stated that action under section 39(2) can be triggered on an event which ought to be intrinsic to the working and functioning of the specific mutual fund scheme. The event indicated in the notice dated 23.4.2020 refers to spread of COVID-19, resultant lockdown and the purported redemption pressures. It is stated that the events narrated in the notice dated 23.04.2020 are all temporary and in any case did not stop or close the debt market which continue to be traded at the exchange. The events narrated are patently extraneous to base a decision of "winding up of a scheme". The schemes in question are all open-ended short-term debt or ultra-short term debt schemes. The schemes were intended to invest in “debt” instruments of companies for a short duration. A decision to wind up, on the stated events of spread of the virus or the resultant lockdown is unfathomable.

As per Regulation 39(2)(a) of MF Regulations, the decision of the trustees to wind up a scheme is not unilateral but is subject to approval by the unit-holders under Regulation 41. The decision of the trustees regarding their satisfaction on the "happening of the event" under Regulation 39(2)(a) is subject to scrutiny such that it must be considered and approved by the unit-holders in the meeting required to be conducted under Regulation 41 MF Regulations, however, no such meeting has been called upon till date. The unit-holders were never called upon to authorize the trustees or any other person to take steps for winding up of the scheme. Further, no satisfactory explanation has come forward explaining the circumstances which necessitated the extreme step of winding up. It becomes the duty of the AMC and the Trustees to explain as to why other avenues could not be availed of by the trustees to improve liquidity or to explain the reasons which had resulted in the failure of the scheme so as to call for their winding up.

The unit-holders have a right under section 61 of the Indian Trusts Act, 18825 to compel the trustee to perform any particular act of his duty. It is stated that where the beneficiary requires a fund house to seek approval of its decision to wind-up, the trustee cannot refuse the same and the trustees must seek the approval of the unit-holders of their decision to wind-up the schemes by explaining the reasons which necessitated such drastic action. Section 61 provides as follows:

"61. Right to compel to any act of duty.-

The beneficiary has a right that his trustee shall be compelled to perform any particular act of his duty as such, and restrained from committing any contemplated or probable breach of trust.

Further a trust once created can be revoked only in accordance with section 78 of the Indian Trust Act, sub-section(a) of Section 78 clearly provides that a trust otherwise created can be revoked, where the beneficiaries are competent to contract, by their consent. Section 78 provides as follows:

78. Revocation of trust. - A trust created by will may be revoked at the pleasure of the testator.

A trust otherwise created can be revoked only-

(a) where all the beneficiaries are competent to contract -- by their consent;

(b) where the trust has been declared by a non-testamentary instrument or by word of mouth--in exercise of a power of revocation expressly reserved to the author of the trust; or

(c) where the trust is for the payment of the debts of the author of the trust, and has not been communicated to the creditors--at the pleasure of the author of the trust.

It is worth mentioning here that in view of Section 32 of the SEBI Act, 19926 which provides as under, section 78 of the Indian Trusts Act, 1882 would continue to apply and its provisions are to be read along with the regulations which do not contain any provision which bars approval of our clients and other unit holders being the only beneficiaries of the decision of the Trustees to wind up the schemes.:

5http://agritech.tnau.ac.in/ngo_shg/pdf/indian_trusts_act_1882.pdf

6https://www.sebi.gov.in/acts/act15ac.html

"32. Application of other laws not barred.- The provisions of this Act shall be in addition to, and not in derogation of, the provisions of any other law for the time being in force."

Another noteworthy aspect is that despite specific promise made by the AMC in its Notice dated 23.04.2020 as well as certain emails received by the investors in this regard and also in utter violation of Regulation 41 of the MF Regulations, no approval has been sought from unit-holders till date. The said regulation 41 provides as under:

"41. Procedure and manner of winding up - (1) The trustee shall call a meeting of the unit-holders to approve by simple majority of the unit holders present and voting at the meeting resolution for authorising the trustees or any other person to take steps for winding up of the scheme:

Provided that a meeting of the unit-holders shall not be necessary if the scheme is wound up at the end of maturity period of the scheme."

No voting either through electronic or any other means has taken place till date. As per Regulation 41, meeting cannot be called electronically in view of the requirement which provides that the unit-holders 'present and voting at the meeting' to approve by simple majority a resolution for taking steps for winding up of the scheme. In the present circumstances, due to lockdown of the entire country, by an executive order issued under the provision of Epidemic Diseases Act, 1890 as well as the National Disaster Management Act, 2005, which has extremely curtailed movement of people from one part of the country to the other, a meeting in terms of Regulation 41 cannot be called as a result of which the exercise will become futile.

The investors had instilled their trust in Franklin Templeton owing to its global investment insight. Even during the pandemic (Covid-19) when the trend in the market was withdrawal of money, certain investors had relied on the statement made by Mr. Santosh Kamath, who is the key manager of the funds, in the “market insight” commentary giving the impression that the AMC is on top of the higher redemptions. In the own official Franklin

Templeton document, under a section titled "Opportunities Ahead", it had been stated, "Even at shorter end products like Franklin India Ultra Short Bond Fund provide great investment opportunity."7 Such statements have been made as late as April 16, 2020 and the mutual funds were highly recommended and were portrayed to be a safe investment. Thus, relying on such statements, many investors kept their money invested, only to be deceived now. Such statements released in public domain resulted in breach of trust of the investors.

At this juncture, it becomes imperative to reproduce Section 409 and Section 418 of the Indian Penal Code, 1860 and simply ponder if the same can be made applicable to the facts and circumstances of the present case:

"409. Criminal breach of trust by public servant, or by banker, merchant or agent.- Whoever, being in any manner entrusted with property, or with any dominion over property in his capacity of a public servant or in the way of his business as a banker, merchant, factor, broker, attorney or agent, commits criminal breach of trust in respect of that property, shall be punished with imprisonment for life, or with imprisonment of either description for a term which may extend to ten years, and shall also be liable to fine.

418. Cheating with knowledge that wrongful loss may ensue to person whose interest offender is bound to protect.- Whoever cheats with the knowledge that he is likely thereby to cause wrongful loss to a person whose interest in the transaction to which the cheating relates, he was bound, either by law, or by a legal contract, to protect, shall be punished with imprisonment of either description for a term which may extend to three years, or with fine, or with both."

It is pertinent to mention here that certain investors have recently received email giving details of the 'voting' that Franklin Templeton intends to conduct. In said email, which has been written by Mr. Sanjay Sapre, it has been mentioned "If Trustees do not receive authorization to proceed with disposal of assets of the scheme, this may delay the process of monetizing such assets and distribution of proceeds." It is to be noted that since the voting is to be done in accordance with Regulation 41 of the MF Regulation, it is difficult to understand how such an interpretation i.e. delay in case of negative outcome, is arrived at. Since, the regulations does not

contemplate any delay in winding-up, it can be presumed that again a mis-statement is being made by the AMC so as to make the investors vote in the favour of the Trustees. Such an action by one of the largest AMCs was not expected.

For the investors to gain their trust back into the AMC, it becomes imperative for the AMC to focus on returning the funds as soon as possible. In case the same is not done, it will have both long term and short term negative repercussions on the various schemes offered by Franklin Templeton in Indian market. In case of any further advice, with respect to the remedies available with the investors, they can contact the authors via any of the following modes:

Website: http://www.lexcommerci.com/

Email: rm@LexCommerci.com

Authored By: Adv. Raghujeet S. Madan & Adv. Sonia Madan

© 2020 Lex Commerci. All Rights Reserved.

Designed By AMS Informatics